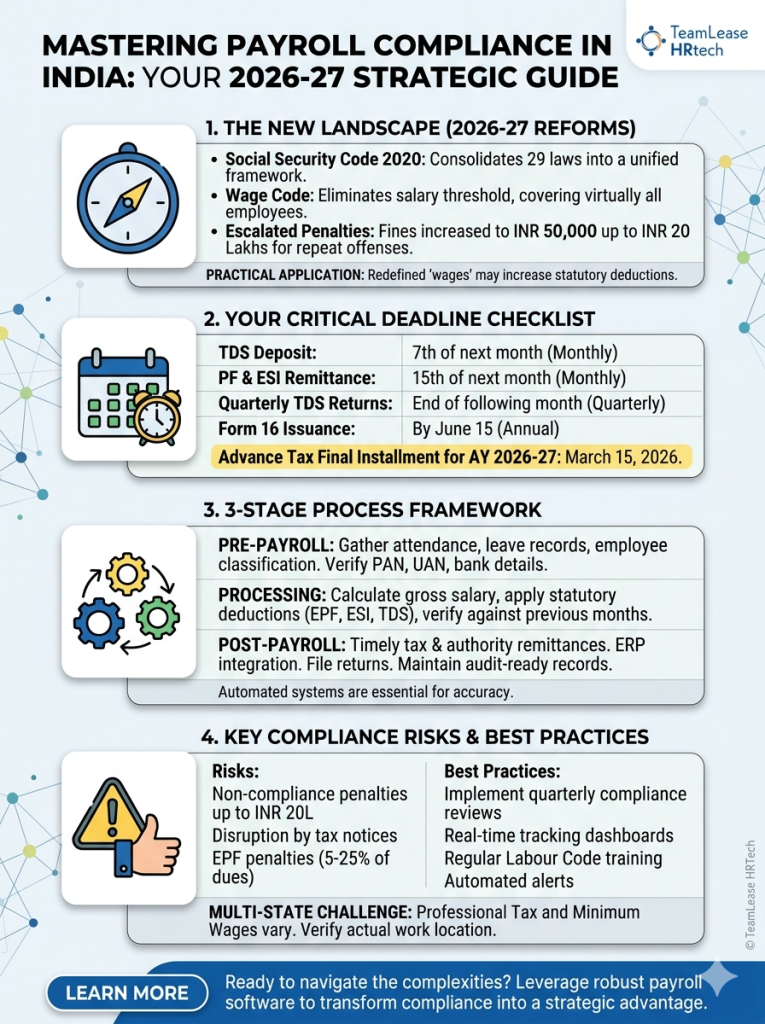

The landscape of payroll compliance in India has transformed dramatically with sweeping reforms taking center stage in 2026-27. Employers today face unprecedented scrutiny, with penalties escalating to INR 50,000 to INR 20 lakhs for repeat offences and interest charges under sections 234B and 234C of the Income Tax Act. This comprehensive guide navigates the complexities of statutory compliance in Indian payroll, ensuring your organization remains compliant while avoiding costly penalties.

Why Statutory Compliance in Indian Payroll is Non-Negotiable in 2026-27

Statutory compliance in Indian payroll refers to the mandatory adherence to central and state labor laws governing employee compensation, deductions, and welfare. Key legislation includes the Income Tax Act, EPF Act, ESI Act, and the transformative Code on Wages 2019. The game-changer for 2026-27 is the Social Security Code, notified in November 2025, which consolidates 29 separate legislations into a unified framework.

This multi-layered system encompasses salary calculations, statutory deductions (Provident Fund, Employee State Insurance, Tax Deducted at Source), timely deposits and filings, and meticulous record-keeping. The shift from pre-2026 regulations is significant—where the Payment of Wages Act previously applied to salaries under INR 24,000, the Wage Code eliminates this threshold, bringing virtually all employees under its purview.

Employers must navigate both national regulations and state-specific variations, including professional tax and minimum wage requirements. For organizations with 20 or more employees, EPF and ESI compliance becomes mandatory. The standard 12% EPF contribution (split between employee and employer on basic salary plus dearness allowance) and ESI rates (0.75% employee, 3.25% employer for wages below INR 15,000 per month) form the foundation of this compliance framework.

Critical Deadlines at a Glance

| Compliance Item | Deadline | Frequency |

|---|---|---|

| TDS Deposit | 7th of next month | Monthly |

| PF & ESI Remittance | 15th of next month | Monthly |

| Quarterly TDS Returns | End of following month | Quarterly |

| Form 16 Issuance | June 15 | Annual |

Core Statutory Deductions and 2026 Labour Code Updates

Under the 2026 new wage codes, statutory deductions remain the foundation of payroll compliance, but the definition of “wages” has significantly tightened. The Employee Provident Fund (EPF) requires a dual contribution of 12% from both employees and employers. However, this is no longer calculated simply on Basic and Dearness Allowance; it must now be calculated on a “wage” base that constitutes at least 50% of the total remuneration (CTC). If allowances exceed half of the total pay, the excess is added to the calculation base.

This mandate applies to all establishments with 20 or more workers. As per standard procedure, the employer’s 12% contribution continues to be bifurcated between the Employee Provident Fund (EPF) and the Employee Pension Scheme (EPS), ensuring higher long-term social security at the cost of slightly adjusted monthly take-home pay.

Employee State Insurance (ESI) provides medical and cash benefits to workers earning gross wages up to INR 21,000 per month. The contribution structure comprises 0.75% from employees and 3.25% from employers on the total gross salary. Tax Deducted at Source (TDS) follows monthly withholding as per the applicable income tax slabs under the latest Finance Act, requiring precise calculation and timely deposit to ensure regulatory compliance and avoid employee grievances.

Additional deductions include state-specific professional tax, labour welfare funds, and statutory bonuses. The bonus threshold, previously capped at INR 21,000 per month, awaits final notification under the new codes.

Impact of New Labour Codes

The Labour Codes 2026 represent India’s most significant labor reform, consolidating 29 laws into four comprehensive codes: Code on Wages 2019, Social Security Code, Industrial Relations Code, and Occupational Safety Code. Key changes include:

- Redefined ‘wages’ calculation for PF and ESI under the Social Security Code, potentially increasing statutory deductions

- Revised standing orders review requirements for establishments

- Escalated penalties ranging from INR 50,000 to INR 20 lakhs for violations

- Streamlined compliance for multi-state operations

For practical application, consider an employee with INR 10,000 basic salary. The EPF contribution would be INR 1,200 from both employee and employer. Employers must generate detailed payslips showing all components: basic pay, House Rent Allowance (HRA), Leave Travel Allowance (LTA), variable pay, meal allowances, gross salary calculation, and final net pay after deductions.

Critical Compliance Deadlines and Payroll Processing Stages

Timely compliance separates successful organizations from those facing regulatory action. The payroll compliance calendar 2026-27 demands precision across multiple touchpoints:

Monthly obligations include TDS deposits by the 7th and PF/ESI remittances by the 15th of the following month. Quarterly TDS returns consolidate three months of deductions, while annual Form 16 certificates must reach employees by June 15 post-financial year. For Assessment Year 2026-27, the final advance tax installment falls on March 15, 2026, applicable to companies, LLPs, and professionals. Special TDS provisions under sections 194M, 194IA, 194IB, and 194S require January-February challans by March 2, 2026.

Three-Stage Payroll Processing Framework

Pre-Payroll Stage: Gather attendance records, leave applications, employee classification data, and verify documentation (PAN, Aadhaar, bank details, appointment letters, salary structures, Universal Account Numbers, ESIC numbers). This foundational stage prevents downstream errors.

Processing Stage: Calculate gross salary, apply statutory deductions, verify calculations against previous months, and generate payslip components with complete transparency. Automated systems reduce manual errors significantly during this critical phase.

Post-Payroll Stage: Execute timely remittances to tax and statutory authorities, integrate accounting entries into ERP systems, file mandatory returns, maintain audit-ready records, and ensure Digital Signature Certificate (DSC) validity for electronic filings.

Navigating Multi-State Payroll Compliance Challenges

While central laws like EPF and ESI maintain uniformity nationwide, multi-state payroll compliance introduces significant complexity through state-specific regulations. Professional tax varies dramatically—Maharashtra imposes different slabs than Karnataka, and some states exempt this levy entirely. Labour welfare fund contributions and state minimum wage regulations add additional layers of compliance.

The rise of remote and hybrid workforces amplifies these challenges. An employee working remotely in Bangalore while employed by a Mumbai-based company triggers Karnataka’s labor laws, not Maharashtra’s. Organizations must verify actual work locations rather than assuming headquarters jurisdiction applies universally.

| Compliance Type | Uniformity Level | Key Variations |

|---|---|---|

| EPF/ESI | Uniform Nationally | First time employee, EPS applicability |

| Professional Tax | State-Specific | Rates, exemptions, thresholds |

| Minimum Wages | State-Specific | Industry, skill level, geography |

Maintain comprehensive documentation including salary registers, attendance logs, tax computation reports, payment challans, payslips, and bonus/gratuity calculations to ensure audit-ready records across all operating states.

Penalties, Risk Mitigation, and Best Practices

Non-compliance carries severe consequences: interest charges accumulating daily, tax notices disrupting operations, fines reaching INR 20 lakhs, and EPF penalties ranging from 5-25% of dues. The Labour Codes 2025 mandate salary payment by the 7th of the following month, with violations attracting substantial penalties.

Implement a robust payroll compliance checklist 2026 covering pre-payroll verification (attendance accuracy, employee classification updates), processing controls (dual calculation verification, deduction validation), and post-payroll governance (deadline tracking, periodic internal audits, reconciliation with statutory accounts).

Best practices include:

- Quarterly compliance reviews with finance and HR teams

- Real-time deadline tracking dashboards

- Regular training on Labour Code updates

- Documentation protocols for leave encashment and flexible benefits

- Automated alerts for upcoming filing dates

Top Payroll Software and Tools for Seamless 2026 Compliance

Technology has become indispensable for managing statutory compliance in Indian payroll. Leading solutions offer comprehensive automation:

WalletHR excels in multi-state support, automating the complete compliance checklist from calculations through filings. Its deadline tracking system and employee self-service portals reduce administrative burden while maintaining audit-ready documentation.

It integrates payroll with broader ERP functionality, handling calculations, payslip generation, statutory remittances, and accounting entries seamlessly. This unified approach eliminates data reconciliation issues between systems.

We cater to organizations with global operations, managing India-specific tax, PF, ESI, and state compliance. Its audit trail capabilities provide comprehensive compliance evidence.

For startups and scaling organizations, automated payroll systems transform compliance from a risk liability into a competitive advantage, ensuring accuracy while freeing resources for strategic initiatives. The investment in robust payroll software pays dividends through penalty avoidance and operational efficiency.

Conclusion

Navigating statutory compliance in Indian payroll for 2026-27 requires vigilance, expertise, and the right technological infrastructure. The consolidated Labour Codes, escalating penalties, and multi-state complexities demand proactive compliance strategies. By implementing comprehensive checklists, leveraging automation, and maintaining meticulous records, organizations can transform compliance from a burden into a foundation for sustainable growth. Stay ahead of regulatory changes, invest in capable systems, and prioritize accuracy—your organization’s reputation and financial health depend on it.